Write something

12d •

How to Trade Gold Strategically Right Now (3 Trade Ideas)

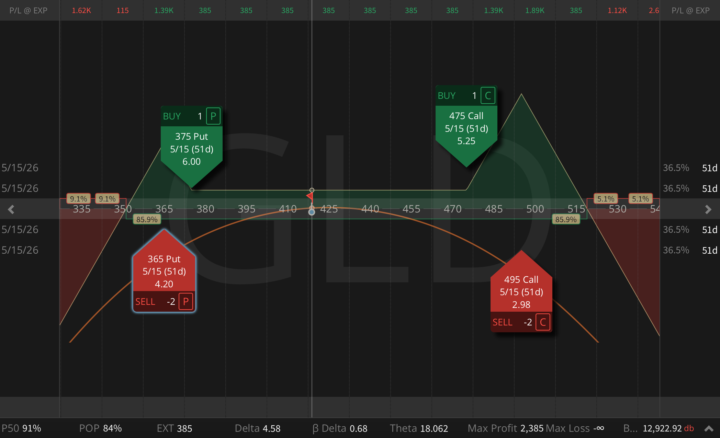

Gold just posted its worst weekly decline in over 40 years, during an active Middle East war, with oil in triple digits and the Strait of Hormuz partially closed. Every macro textbook says that combination is powerfully bullish for gold, but instead, spot dropped roughly 20% from the all-time high. In my view, this was not a fundamental repricing of gold's long-term value. This was a forced deleveraging event. The oil shock drove inflation expectations high enough to keep the Fed hawkish, real yields stayed positive, the dollar surged, and months of crowded, leveraged long positioning (expressed heavily through structures targeting 5,500-6,000) unwound into thin overnight books. Order depth on COMEX reportedly collapsed by over 90% during the worst session. So I see this as a liquidity cascade. The critical tell; equities VIX is sitting in the high 20s. GVZ (the gold vol index) spiked above 43 last week, a 55% move in five days, to levels last seen during the 2020 pandemic panic. Gold volatility is now trading at a ratio to Treasury volatility last seen just before the 2008 Lehman collapse. That spread is a volatility surface that is still pricing a crash that has already happened. Below are three structures I'm using right now, all in GLD and all expiring 5/15, to monetize that dislocation in three different, but very smart and strategic, ways. Trade 1: The Double Batman Structure: Buy 1 x 380 Put / Sell 2 x 360 Put / Buy 1 x 475 Call / Sell 2 x 505 Call, all 5/15 (51d) Net credit: $815, Probability of Profit: 87%, Max Profit: $3,815, Theta $36/day This is the broadest and most neutral of the three setups, built around one core idea, that GLD stays inside a wide consolidation range while implied volatility mean-reverts. I'm selling inflated premium on both wings of the surface, while keeping a defined body inside the trade and leaving the far tails for active management (if needed). The payoff shape creates two separate profit humps, which is why I call it the Double Batman. I'm harvesting premium that is still stranded in both tails after the recent liquidation event, while gold itself is trying to stabilize.

4d •

SPY Risk-Free Butterfly

We did it again! If you follow, on March 23 we opened a SPY 640/620 put ratio spread for a $598 credit. Yesterday, I bought the 600 put for $4.77 and turned the entire position into a RISK-FREE butterfly. Now the trade has: - No downside risk - No upside risk - Locked-in profit: $121 - Max profit: $2,121 This is how short volatility works when we stop thinking directionally and start thinking in structures.

14d •

Everyone's Celebrating the Rally, I'm Selling What They Still Fear

What Just Happened Just before a 48-hour ultimatum expired, Trump announced via Truth Social he's postponing U.S. strikes on Iranian power plants for five days, describing talks as "very good and productive". A complete reversal from his weekend threat to obliterate Iran's power grid. Markets exploded higher; S&P +2.2%, Nasdaq +2.17%, brent crude collapsed over 10%. VIX, which spiked above 30 earlier as markets priced in $150 oil, came off hard, and energy gave back everything. Tech and transport surged. The catch nobody's talking about is the ultimatum clock was reset, not cancelled. This rally is priced on a five-day promise with zero structural resolution! Skew is off its highs but still elevated. That gap between spot complacency and residual volatility premium is exactly where my trade lives. My Position SPY Put Ratio Spread: Buy 1 x 640 Put, Sell 2 x 620 Puts (all 53 DTE), Net credit: $598, Max Profit: $2,598, Probability of Profit: 89% (!) I'm not fading the rally or betting on re-escalation, I'm just selling the fear that's still priced into the downside strikes while the market is already repricing toward relief. Those are two different things moving at two different speeds right now. If the rally holds, I keep the full credit. If we give back some gains without collapsing, the position drifts toward maximum profit. If implied volatility continues to compress, theta and vega work in my favor simultaneously. And importantly: if we drift into that 620 area, this structure can deliver up to $2,600 profit. So three independent paths to a winning outcome. We only need one. Tail risk is managed according to the Trading Plan, and if needed, this structure naturally transitions into further premium-selling cycles. Stay tuned.

1

0

18d •

Learn to Trade the IV Crush the Right Way (ACN Earnings, 3 Ideas)

There is one of the most consistently profitable edges in options trading: earnings volatility. It is backed by years of academic research, it repeats every single quarter across hundreds of names, and still most traders approach it the wrong way. Done correctly, earnings trades can become the backbone of a highly repeatable income stream. You're not gambling on direction; use a structured approach that puts probability in your favor. Today I'll show you exactly how I apply that framework to a live setup. ACN reports earnings after the bell, and below are three specific trade ideas built around the same edge. Most traders look at a large implied move, assume the market is overpricing the event, and sell a strangle. It works. Until it doesn't. And one loss will erase months of careful premium collection. That is because your real edge is not in blindly selling premium, but in understanding that earnings distort the term structure in a very specific and very tradable way. The expiration that contains the announcement gets loaded with huge event premium, and the next expiration out contains far less of it. After the print, the front-week premium collapses immediately, and the deferred week crushes much less. That spread between expirations is one of the most consistent opportunities in options, validated by thousands of backtests and academic research. For Accenture (ACN), the 3/20 expiration is carrying the event risk, the 3/27 expiration is not. That gives us a clean surface distortion to target. And here are three ways to trade it, depending on how strong your directional view is. Trade 1: Bullish Diagonal Structure: Sell 1 x 210 Call, expiring 3/20, Buy 1 x 205 Call, expiring 3/27. This is the cleanest and most repeatable setup of the three, because you are selling the most inflated part of the surface, and buying a slightly lower-strike call in the next expiration, where IV should hold up much better after the print. The long 205 call sits below the short 210 call, which gives the structure a bullish shape.

2

0

26d •

7 of 30 Real Trade Ideas from Our Fund

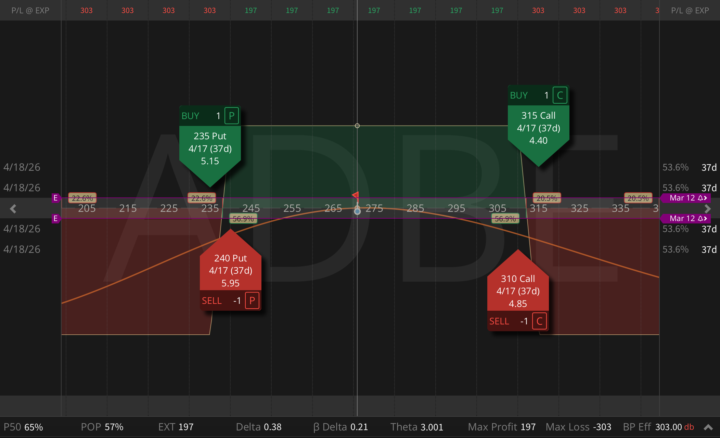

As you know, when I present trade ideas here, I usually go very deep into the analysis. Each position is built on multiple layers of research: fundamentals, implied volatility levels, volatility surface (both skew and term structure), liquidity, and additional signals I track and I'll share in the posts here. The goal is always to identify trades with strong premium, high probability, and structures that are relatively easy to manage. But today I decided to do something a little different. After our latest fund portfolio meeting and internal discussion, we opened 30 new trades across the portfolio. Instead of writing a long analysis for each one, I will simply show you 7 of those trades exactly as they were placed. Below are 7 of the 30 new positions currently running in our portfolio. 1. ADBE Iron Condor Structure: Buy 235P / Sell 240P / Sell 310C / Buy 315C (37 DTE) Premium collected: $197; POP: 57%; P50 probability: 65%; Beta-weighted delta: +0.21; Theta: +$3/day; Max profit: $197; Max loss: $303 2. COIN Iron Condor Structure: Buy 130P / Sell 140P / Sell 240C / Buy 250C (65 DTE) Premium collected: $350; POP: 61%; P50 probability: 74%; Beta-weighted delta: -1.61; Theta: +$3.28/day; Max profit: $350; Max loss: $650 3. CRM Put Ratio Spread Structure: Buy 185P / Sell 2x175P (37 DTE) Credit received: $117; POP: 86%; Beta-weighted delta: +3.91; Theta: +$9.73; Max profit: $1,117 4. NKE Naked Put Structure: Sell 50P (65 DTE) Premium collected: $152; POP: 75%; P50 probability: 86%; Beta-weighted delta: +2.22; Theta: +$2.47; Max profit: $152 5. PEP Strangle Structure: Sell 145P / Sell 170C (37 DTE) Premium collected: $279; POP: 71%; P50 probability: 83%; Beta-weighted delta: -0.69; Theta: +$9.70; Max profit: $279 6. AMD Put Credit Spread Structure: Buy 180P / Sell 190P (37 DTE) Premium collected: $262; POP: 66%; P50 probability: 78%; Beta-weighted delta: +5.37; Theta: +$2.03; Max profit: $262 7. VISA Risk-Free Butterfly (Synthetic Bonds with Lottery Ticket)

1

0

1-28 of 28

powered by

skool.com/options-jive-1159

STOP trading market direction. Start using options strategies to turn volatility into steady income. We sell premium, and think in probabilities.

Suggested communities

Powered by