Write something

Pinned

Feb 8 •

🚀 Welcome to the 700 Club! Start Here (Action Required)

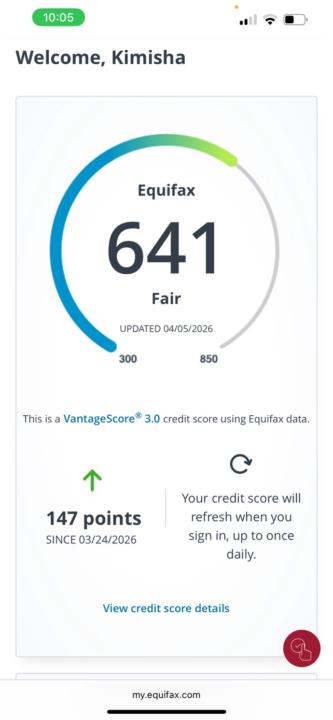

Peace and Strength Team! Welcome to the inner circle. You aren’t just here to “fix your credit”—you’re here to master the system and unlock the lifestyle you deserve. Whether you’re at a 400 or a 650, the goal is the same: Tier-1 Credit and Financial Freedom. Most people fail because they use outdated templates and "free" apps that actually hurt their scores. In this community, we do things differently. We use Metro 2 compliance—the same "federal code" the banks use—to force the bureaus to play by the rules. Where to start right now: Watch the Masterclass: I’ve uploaded a step-by-step presentation (find it in the Classroom tab) that breaks down exactly how to audit your report. Download the Checklist: Get your 400 to 700 Roadmap (attached below). Print it out. This is your battle plan for the next 45 days. Claim Your Gems: Check the "Weekly Letters" section for this week’s free dispute templates. Introduce Yourself: Post a quick "Hello" in the feed! Tell us: What is your goal score? What is the first thing you’re going to do once you hit 700+? (New home? Better car? Business funding?) The Bonus Perks: Don’t forget, as a member, you get access to our 1-on-1 Book Calls and our Weekly Credit Consultations. If you get stuck, the community and I are here to pull you through. The bureaus are betting that you’ll get bored and quit. We’re betting that you’ll stay consistent and win. Let’s get to work. See you in the feed, Samiel Quijano

4d •

Did You Know ??

The "First" Constitution (1787/1789) The first constitution is the Constitution for the United States of America. Status: This is viewed as the "organic" or "foundational" document of the Republic. The Key Distinction: It established a government of limited powers, where the people were the "principals" and the government was the "agent." The Money: Under Article I, Section 10, only gold and silver coin were to be used as tender in payment of debts. 2. The "Second" Constitution (1871/1933) The theory suggests that a "second" constitution—the CONSTITUTION OF THE UNITED STATES (all caps)—was created to govern the "Corporation" established in 1871. The 1933 Event: This refers to the Emergency Banking Act and House Joint Resolution 192 (HJR 192). The Claim: In 1933, the U.S. went "bankrupt" to the Federal Reserve. Because the government removed gold as a way to pay debts, they allegedly "incorporated" the citizenry's future labor as collateral. 3. How This Impacts Consumer Law (The "Secret") From a forceful consumer protection standpoint, 1933 is the year "Payment" was replaced by "Discharge." The Theory: Since there is no "real" money (gold/silver), you cannot technically "pay" a debt; you can only "discharge" it using the government's credit (Federal Reserve Notes). The Legal Force: This is why "Verification of Debt" is so powerful. If a debt collector cannot prove they gave you "lawful money" (gold) in exchange for your signature, they are technically trading on your credit, not theirs.

4d •

yooo , i crack the code.( READ THIS )

The Triple-Threat Dispute Strategy 1. The Demand for Substance (Wet-Ink Signature) - The Logic: In a post-1933 "credit-based" system, the only thing that creates "value" is your signature. If they don't have the original contract, they are essentially reporting a "debt" based on air. - The Law: UCC § 3-305 and 15 U.S.C. § 1692g. - The "Force": "If you cannot produce the original instrument of indebtedness, you have no 'Standing' to report this claim on my private consumer profile." 2. The Demand for Ownership (Chain of Title) - The Logic: Debt is often sold 5 or 6 times. If a collector is missing even one "Assignment of Debt" (the Bill of Sale), they are legally a stranger to the account. - The Law: UCC § 3-302 (Holder in Due Course). - The "Force": "Provide a notarized Chain of Title from the Original Creditor to your organization. A digital summary is not a legal transfer of rights." 3. The Demand for Process (Method of Verification - MOV) - The Logic: Bureaus use "e-OSCAR" to verify accounts in seconds. This is a "Corporate Error" because a computer cannot "reasonably reinvestigate" a legal dispute. - The Law: 15 U.S.C. § 1681i(a)(6) & (7). - The "Force": "I demand the name, address, and telephone number of the person who personally verified this data. Failure to provide this information within 15 days is a statutory violation of the FCRA."

1

0

1-30 of 54